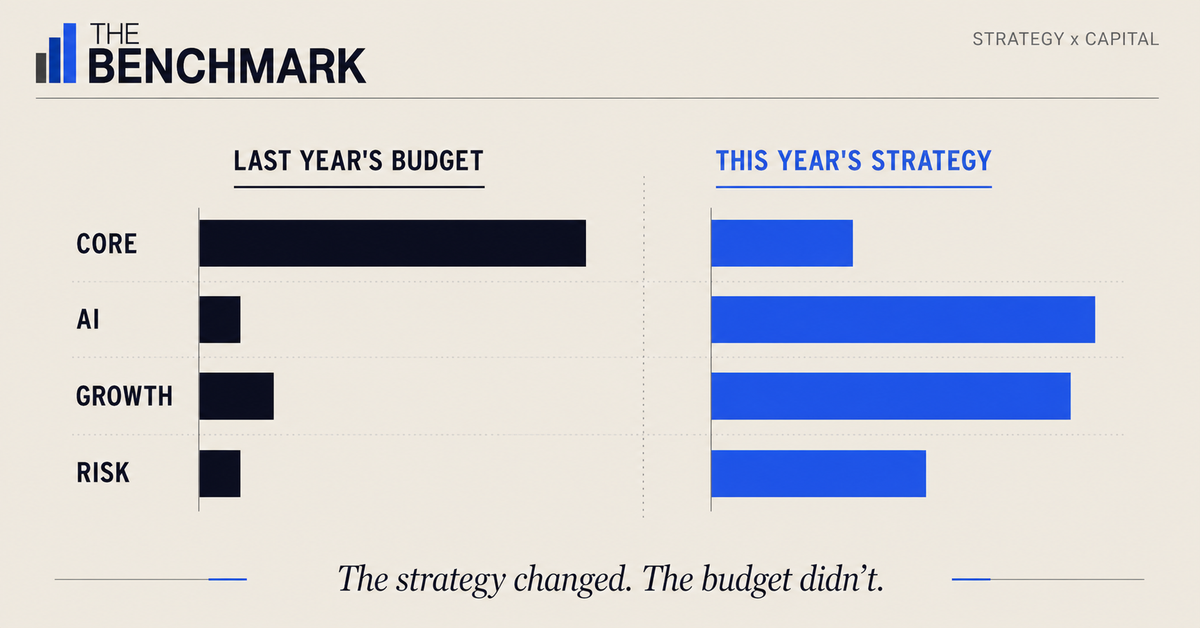

You're Funding Last Year's Strategy With This Year's Money

The annual budget was designed to close arguments. The market did not agree to stop moving.

You approved the budget in November. By February, parts of it were already wrong.

The market had moved. A competitor had changed pricing. A customer segment had slowed. A new AI capability made one initiative more urgent and another less defensible. Everyone could see it. No one had a clean mechanism to act on it.

That is not a planning failure. It is the annual budget working as designed. The process exists to resolve conflicts, protect commitments, and provide every function with a defensible allocation. It is much less effective at keeping capital in motion after reality changes.

This is how organizations end up funding last year's strategy with this year's money. Not because leaders lack insight. Because the system gives old commitments an advocate in every room and gives new priorities a business case they must fight to prove.

The result is resource inertia: the tendency of capital, talent, and executive attention to remain attached to prior decisions long after the strategic logic has weakened.

Table of Contents

The Budget Is a Conflict-Resolution Device

The annual budget has industrial origins. It was built for environments where assets were fixed, demand was more predictable, and the managerial challenge was cost control across a stable portfolio. It was not designed to continuously reallocate capital toward an uncertain future. It was designed to defend an already committed present.

That design persists because it solves a real organizational problem. It closes the argument.

Every function gets a forum. Every leader gets a number. Every stakeholder gets a moment to negotiate. Once the envelope closes, the organization receives something valuable: a shared fiction of certainty.

The market does not close with it. Customers keep moving. Competitors keep repricing. Technology keeps changing the cost curve. The budget becomes a frozen answer to a question that has already changed.

That bias quietly favors incumbents. Existing programs have teams, metrics, historical approvals, and sunk-cost logic. New priorities have urgency, but urgency is not the same as ownership. In a compressed annual negotiation, history has more advocates than strategy.

The organization ends up with a portfolio that reflects what it used to believe more than what it now needs to do.

Resource Inertia Is the Real Strategy

Most companies do not mean to let the budget become the strategy. It happens because resources are the only strategy the organization can actually execute.

A new priority is announced. The slide deck is clear. The CEO repeats it. The town hall lands well. Then the work enters a resource system still optimized around last year's commitments. The new initiative receives a small fund, a borrowed team, or a leadership sponsor without the authority to move anything material.

Six months later, the priority underperforms. It was too new, too cross-functional, too dependent on teams whose incentives still pointed elsewhere. A review is convened. The old programs defend their base. The new priority defends its promise. Everyone leaves with something. The strategy leaves the least.

Bain's 2024 transformation research found that 88% of business transformations fail to achieve their original ambitions. The common failure is not that the strategy was incomprehensible. It is that the resource base never shifted enough to make the strategy real.

The academic mechanism is older than the current planning cycle. Barry Staw's work on escalation of commitment described the tendency to keep investing in prior decisions because reversing them would make earlier judgments visible. Teams defend what they built. Managers protect what they approved. Executives avoid the political cost of reversal. Six months later, the same meeting happens again.

Researchers call this resource inertia. Most executives call it planning.

Reallocation Velocity Is the Missing KPI

The performance cost is measurable.

McKinsey's research across more than 1,500 companies found that organizations in the top quartile of capital reallocation activity generated roughly twice the returns of those with static allocations. The annual difference, approximately 10% average shareholder return versus 6%, compounds into a major value gap over time.

BCG's analysis of capital allocation behavior found that many companies exhibit proportional allocation, distributing capital based on business unit size rather than strategic potential. Outperformers invested more aggressively where capital could create value and pulled away faster where it could not.

Gartner's Run, Grow, Transform framework captures the internal version of the same problem. Most organizations allocate the majority of their technology and operating budgets to running what already exists. Run crowds out, Grow. Grow crowds out Transform. The work that changes the long-term position receives what remains after every incumbent claim has been honored.

This is why reallocation velocity should be treated as a strategic KPI. It measures the percentage of capital and talent actively shifted across priorities over a rolling period. It is not a perfect metric. It is a useful warning light.

If the strategy has changed but reallocation velocity has not, the strategy has not changed. It has been narrated.

The Danaher Proof Point

Danaher is a useful example because the lesson is not simply that the company reallocates capital. It is that reallocation is embedded in an operating system.

The Danaher Business System, documented in Harvard Business School case research, relies on frequent operating reviews, disciplined measurement, and explicit management routines that surface underperformance and redirect resources before the annual calendar demands it. The company does not wait for a once-a-year planning ritual to decide whether a business unit, acquisition opportunity, or operating priority deserves capital.

The point is not chaos. It is optionality.

When an acquisition window opens, the decision infrastructure is already in place. When a business unit underperforms its strategic thesis, the review cadence surfaces the problem before another annual budget locks the situation in place. When a growth area earns capital, the organization has a mechanism to move resources without turning each decision into a political crisis.

The lesson is not to copy Danaher. It is to recognize that companies with high reallocation velocity are not relying on executive instinct. They have a meeting, a mandate, and a decision-making structure that enables movement.

Most organizations have a meeting. They do not have the mandate.

Where This Argument Gets Complicated

The objection is real: rapid reallocation can become a form of dysfunction in its own right.

Organizations have finite change capacity. Teams cannot absorb infinite pivots. Constant movement can produce fatigue, strategic confusion, and underinvestment in capabilities that require sustained commitment. Some businesses need long-cycle investment discipline precisely because the return does not appear inside a quarterly review window.

That is why the argument is not for aggressive allocation. It is for dynamic allocation.

Aggressive allocation moves capital because movement looks like action. Dynamic allocation reallocates capital when evidence indicates that the current portfolio no longer aligns with the strategy. The distinction matters. The goal is not to make the organization restless. It is to prevent it from sleepwalking.

The greater risk for most companies is not that they are moving too fast. It is that they have no legitimate mechanism to move between annual cycles at all. The cost of over-reallocation is visible. The cost of inertia is quieter, and usually larger.

Implications for Leaders

Run the portfolio review as a standing quarterly decision meeting.

A portfolio review that can observe but cannot move resources is a status update. The review needs authority to stop, shrink, protect, and fund work. Its agenda should be simple: what is underperforming against its strategic thesis, what would be funded if capital were available, and what should stop so the new work can start.

Separate Run, Grow, and Transform before negotiation starts.

When all capital competes in one pool, Run wins. It has existing teams, existing contracts, and existing metrics. Grow and Transform need protected pools with different time horizons and different proof standards. Otherwise, the future enters every meeting already underfunded.

Treat the prior-year budget as a hypothesis.

The default question in most planning cycles is how much to increase or decrease last year's allocation. The better question is whether the company would fund the same work at the same level if it were making the decision today. Some answers will still be yes. The value is in forcing the argument.

Measure reallocation velocity.

Most organizations measure whether existing programs performed. Few measure whether the portfolio's composition is changing. Reallocation velocity gives leaders an early signal that the resource base is moving with the strategy, or that the organization is still defending history.

Make continuation costs visible.

Stopping a program is politically costly because the decision is public. Continuing it often feels free because the cost is buried in the baseline. Place continuation costs ahead of the review committee every quarter. The burden of proof should apply to retaining capital, not merely to requesting it.

The Bottom Line

The annual budget is not the enemy of good strategy. It is a tool built for cost control across a stable portfolio. Most companies are now asking it to do something else: move capital toward a future that keeps changing after the budget closes.

That mismatch creates resource inertia. Old programs keep their funding because they already have owners, metrics, teams, and sunk-cost logic. New priorities arrive with strategic urgency but no structural right to capital. The result is not a dramatic failure. It is a misallocation, quarter after quarter, until the company's resource base no longer aligns with its strategy.

Another planning workshop will not solve it. The missing piece is a live reallocation mechanism with authority, cadence, and permission to stop things. The organizations pulling ahead are not waiting for the calendar to tell them when to move. They set up a meeting that lets them move before the old strategy runs out of the new year.

Sources

McKinsey & Company. "How nimble resource allocation can double your company's value." August 2016. https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/how-nimble-resource-allocation-can-double-your-companys-value

McKinsey & Company. "How quickly should a new CEO shift corporate resources?" October 2013. https://www.mckinsey.de/~/media/McKinsey/Business Functions/Strategy and Corporate Finance/Our Insights/How quickly should a new CEO shift corporate resources

McKinsey & Company. "Resource Allocation for Long-Term Value Creation." May 2024. https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/tying-short-term-decisions-to-long-term-strategy

BCG Henderson Institute. "The Art of Capital Allocation." December 2020. https://www.bcg.com/publications/2023/corporate-development-finance-function-excellence-art-of-capital-allocation

BCG. "Understanding the Importance of Capital Allocation During Crisis." October 2020. https://www.bcg.com/publications/2020/capital-allocation-during-crisis

Gartner. "Run, Grow and Transform the Business IT Spending." 2016. https://www.servicenetwork.org/wp-content/uploads/2016/08/run_grow_and_transform_IT_biz_spend_308477.pdf

Bain & Company. "88% of Business Transformations Fail to Achieve Their Original Ambitions." April 2024. https://www.bain.com/about/media-center/press-releases/2024/88-of-business-transformations-fail-to-achieve-their-original-ambitions-those-that-succeed-avoid-overloading-top-talent/

Barry M. Staw. "The Escalation of Commitment to a Course of Action." Academy of Management Review, 1981. https://journals.aom.org/doi/10.5465/amr.1981.4285694

Harvard Business School. "Danaher Corporation." Case No. 9-708-445. https://www.hbs.edu/faculty/Pages/item.aspx?num=35531