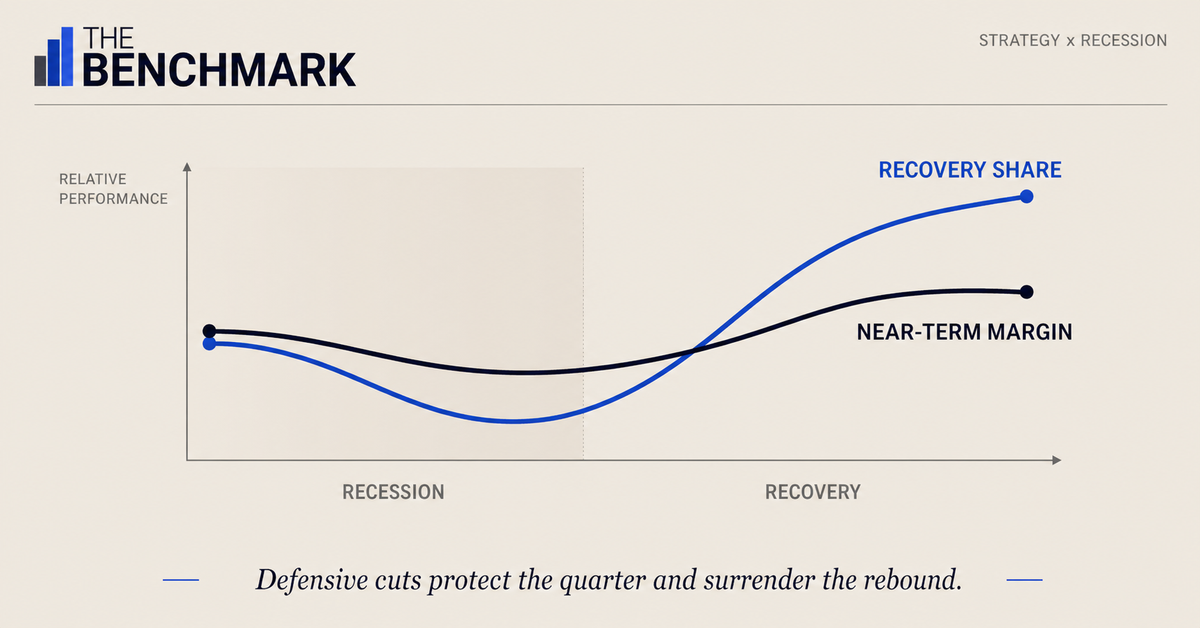

Companies That Play Defense in Recessions Lose the Decade That Follows

Cost discipline is necessary in a downturn. Treating it as a strategy is how companies surrender the recovery.

In early 2026, the corporate instinct is moving toward defense. CFO surveys show recession anxiety, policy uncertainty, delayed capital projects, and tighter spending. The response is understandable. Demand visibility is poor. Tariffs are unsettled. Boards do not reward bravado when margins are under pressure.

But the historical record is not kind to companies that make defense their strategy.

Across four downturns, the pattern repeats. Companies that preserve or increase forward investment during recessions tend to emerge with a stronger market position, better talent, and more durable growth. Companies that cut broadly protect the quarter and weaken the recovery. The difference is not courage. It is capital redeployment.

The strategic error is not cutting costs. Some costs should be cut. The error is treating cost reduction as the destination rather than the source of capital for the bets that determine the next decade.

Table of Contents

The Retreat Is Already Visible

The current moment has all the ingredients that make defensive management feel rational.

Goldman Sachs raised its recession probability in March 2026. CFO surveys from CNBC, Duke University/Federal Reserve, Grant Thornton, and KPMG have all pointed to a similar posture: uncertainty is shaping decisions, investment is being delayed, tariffs are influencing capital plans, and profit expectations have weakened.

The logic is familiar. When visibility falls, leaders protect cash. When policy changes are hard to price, capital projects slow. When the margin is under pressure, discretionary spend becomes vulnerable. Technology pilots are paused. Hiring freezes begin. R&D becomes easier to question.

None of this is irrational in isolation. Companies should preserve financial flexibility. They should cut waste. They should stress-test demand. They should know which investments no longer clear the bar.

The problem is the blanket move: treating all forward investment as optional and all cost reduction as prudent.

That is how companies exit downturns with clean quarters and weaker positions.

The Numbers Do Not Support the Retreat

The evidence across prior cycles is unusually consistent.

Harvard Business Review research on companies during the 2007-2009 recession found that those that increased capital expenditures, economic competencies, and talent investment during the downturn improved across return on equity, sales growth, and market value in the recovery. Companies that decreased investment deteriorated on those same measures.

McKinsey's through-cycle research found that companies outperforming across downturns did not simply cut more effectively. They entered with stronger balance sheets and used the downturn to move. They made more M&A deals. They invested in capabilities. They reallocated resources while competitors were pulling back.

Bain has made a similar point in its recession research: downturns are moments when the game can change because competitors hesitate. Assets become cheaper. Talent becomes available. Customer relationships open. Market share moves.

That is the core misunderstanding. Recessions are not only periods of contraction. They are periods of redistribution.

The companies that benefit are not the ones that ignore risk. They are the ones that distinguish between undisciplined spending and strategic investment.

Why Blanket Cuts Are Self-Defeating

The most dangerous cost program is the one that looks fair.

Across-the-board reductions feel disciplined because every function shares the pain. They also avoid hard prioritization. A 10% cut to every team treats a mature maintenance function, a struggling legacy program, and a high-potential growth initiative as equally adjustable.

That is not a strategy. It is arithmetic.

Blanket cuts damage the future because the easiest things to cut are often the things that create long-term advantage: training, R&D, marketing, product exploration, AI capability building, and early-stage growth bets. Their payoff is uncertain and delayed. Their absence is hard to measure immediately. They lose the budget fight because their value is visible later.

The incumbent base is harder to cut. It has owners, processes, contracts, dependencies, and near-term operating consequences. The future enters the room as a hypothesis. The present enters as an obligation.

That is how downturns quietly preserve the wrong work.

The better approach is selective discipline. Cut what no longer deserves capital. Protect or increase what creates an advantage in the recovery. Use cost reduction as a source of funds, not as the strategy itself.

AI Is This Cycle's Test

Every downturn has a capability question. In this cycle, AI is one of them.

The wrong move is to continue funding every AI experiment because the category is fashionable. The equally wrong move is to pause AI investment broadly because uncertainty has risen.

The useful question is narrower: which AI investments change the operating model, cost structure, product capability, or decision speed in ways that matter after the downturn?

Those investments should not be treated like discretionary spend. They are strategic capacity. The same applies to data infrastructure, process redesign, manager capability, and workflow modernization. Cutting them may help the quarter. It can also leave the organization with less ability to absorb the next expansion.

BCG's research has repeatedly found that companies entering downturns with a more offensive posture can gain an advantage when others retreat. That does not mean spending more everywhere. It means knowing where the next source of advantage is likely to come from and moving capital toward it while competitors are frozen.

The companies that win the recovery often make the uncomfortable investment while the room is still afraid.

Where This Argument Gets Complicated

The obvious counterargument is also the important one: some companies should cut deeply.

If the balance sheet is weak, demand has collapsed, or a company is carrying years of accumulated waste, investment language can become denial. Recessions expose bad economics. Leaders who keep funding everything in the name of offense are not strategic. They are avoiding decisions.

This is not an argument that every company should spend through a downturn. It is important that companies know the difference between survival cuts, efficiency cuts, and strategic cuts.

Survival cuts protect the enterprise. Efficiency cuts remove work that should not exist. Strategic cuts reduce the company's ability to compete after the downturn. The first two can be necessary. The third should be made only with full awareness of the future position being surrendered.

Most companies do not make that distinction clearly enough. They let the pressure of the moment flatten all cuts into discipline.

Implications for Leaders

Separate waste removal from strategic retreat.

Do not describe every cut as discipline. Name what kind of cut it is. If it removes low-value work, good. If it weakens a future capability, say so explicitly and make the tradeoff visible.

Create a list of downturn investments before the panic.

Identify the three to five capabilities, markets, talent pools, or customer segments where a downturn could create an advantage. Decide in advance what evidence would trigger investment, not only what evidence would trigger cuts.

Fund offense with discipline.

Cost reduction should create capital for the few bets that matter. If every dollar saved is consumed by margin protection, the company is not reallocating. It is shrinking.

Protect capability-building work.

Training, AI adoption, workflow redesign, product discovery, and customer insight often look discretionary because they do not directly defend this quarter's revenue. That is exactly why they need explicit protection when the organization tightens.

Watch competitor behavior.

A downturn changes the market map. If competitors pull back on hiring, marketing, R&D, or customer support, their retreat may create an opening. Defensive management often misses these windows because the internal cost agenda consumes the executive calendar.

The Bottom Line

Recessions are not only periods of contraction. They are periods of redistribution. Talent, customers, assets, and attention move when weaker competitors retreat. The benefiting companies are not reckless. They are selective.

The evidence across downturns is clear: cost discipline matters, but it does not create advantage on its own. Advantage comes when leaders use discipline to fund the few investments that will matter after the recovery begins. That may be product capability, AI infrastructure, customer acquisition, M&A, or talent that was unavailable six months earlier.

The companies that play only defense can report clean quarters and still lose strategic ground; they never fully recover. The hard part is not knowing that investment matters. It is making the investment while the room is still afraid.

Sources

CNBC CFO Council Q1 2025 Survey. https://www.cnbc.com/2025/03/25/recession-is-coming-pessimistic-corporate-cfos-say-cnbc-survey.html

Duke University / Federal Reserve Q2 2025 CFO Survey. https://www.highradius.com/finsider/cfos-braces-for-tarrifs-2025/

Grant Thornton Q2 2025 CFO Survey / CFO.com. https://www.cfo.com/news/cfos-slash-profit-forecasts-as-economy-triggers-concern-grant-thornton-2025-q2-cfo-survey-/751036/

Goldman Sachs recession probability / Yahoo Finance. https://finance.yahoo.com/news/goldman-sachs-raised-us-recession-131750734.html

BCG CIO Spending Pulse. https://www.bcg.com/publications/2025/cost-control-now-rivals-growth-as-top-priority

KPMG. "KPMG LLP Survey: U.S. Businesses Grapple with Tariff Fallout." 2025. https://kpmg.com/us/en/media/news/kpmg-survey-tariff-fallout.html

Harvard Business Review. Vijay Govindarajan, Anup Srivastava, and Aneel Iqbal. "Should Midsize Companies Play Offense or Defense in a Downturn?" March 2021. https://hbr.org/2021/03/should-midsize-companies-play-offense-or-defense-in-a-downturn

McKinsey & Company. "Growth Through a Downturn." October 2020. https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/growth-through-a-downturn

Bain & Company. "Using the Next Recession to Change the Game." 2018. https://www.bain.com/insights/using-the-next-recession-to-change-the-game/

Bain & Company. "Offense Is the Best Form of Defense." https://www.bain.com/insights/offense-is-the-best-form-of-defense/

BCG. "The CEO's Guide to Growth in 2026: Seizing Opportunity." January 2026. https://www.bcg.com/publications/2026/the-ceos-guide-to-growth-seizing-opportunity